Why So Many Junior Doctors Get a Surprise PAYG Instalment Notice

A PAYG instalment notice from the Australian Taxation Office can catch junior doctors off guard, particularly after a year in which income has increased through locum work, private billings, or other untaxed income streams. This is because the ATO works out whether PAYG instalments apply based on information reported in your latest tax return.

Importantly, a PAYG instalment notice does not mean you are being taxed twice, and it is not a penalty. The ATO describes PAYG instalments as regular prepayments of the expected tax on business and investment income, collected progressively across the financial year.

This issue often arises when income has been earned without tax being withheld during the year. For doctors, that can include locum income under an ABN, private billing income, or some investment income. Salary and wages paid through payroll are generally covered by PAYG withholding, which is why the instalment notice can feel unexpected when a new income stream is added.

Understanding that distinction can make the notice easier to interpret. In many cases, it reflects how tax is being collected on a different type of income, rather than any new or unexpected category of tax. This guide explains how PAYG instalments work for doctors, when they may apply, and what they can mean in a broader cash flow and tax planning context.

What PAYG Instalments Mean

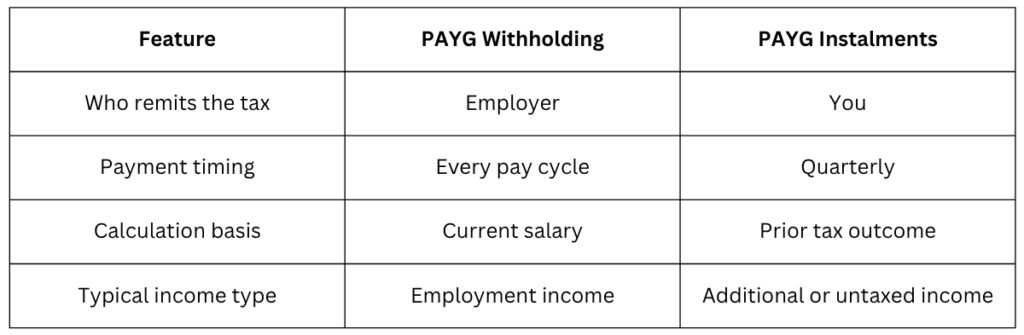

Confusion around PAYG instalments for doctors usually begins with a misunderstanding of how they differ from PAYG withholding. Both relate to income tax, yet they operate through separate mechanisms. Understanding the distinction between the two can reduce unnecessary stress.

PAYG Withholding

PAYG withholding applies to employment income. An employer deducts tax from each pay slip and remits it directly to the ATO. Employment income, including salary and wages paid through payroll, generally falls under PAYG withholding.

The amount withheld is based on ATO tax tables. It is credited against the total tax payable when the annual tax return is assessed. Some junior doctors may only encounter PAYG withholding in the earlier stages of their careers, before adding other income sources.

PAYG Instalments

PAYG instalments apply when income is earned without tax being withheld during the year. Locum income under an ABN, private billing receipts, and certain investment income are common examples. In these situations, PAYG instalments function as regular prepayments of expected tax on business and investment income.

Where a doctor earns business or investment income and meets the ATO’s entry thresholds, the ATO may automatically bring them into the PAYG instalment system. The ATO describes PAYG instalments as a method of paying income tax progressively throughout the financial year. This may help explain why they often arise after a year in which income has increased or become more complex.

Entry generally occurs when tax payable on business or investment income reaches the thresholds set by the ATO. Current ATO guidance indicates individuals, including sole traders, may automatically enter PAYG instalments where their latest tax return shows instalment income of $4,000 or more, tax payable of $1,000 or more, and estimated or notional tax of $500 or more.

How the Prepayment System Works

PAYG instalments paid during the year are credited against your income tax liability when your tax return is lodged and assessed. They are not separate from your tax return. Each amount paid reduces the balance calculated when your income tax assessment is finalised.

If instalments exceed the final tax payable, a refund may be issued. If they are lower than the assessed liability, the difference becomes payable. The system adjusts timing rather than increasing total tax.

Doctors moving from salary-only roles into mixed income arrangements may encounter PAYG instalments for the first time. The structure reflects previous earnings patterns, not a new category of tax. Understanding how the ATO applies these rules can help doctors interpret PAYG instalments in a broader tax context.

When Junior Doctors Usually Enter PAYG Instalments

Questions around PAYG instalments for doctors may relate to when they first apply. Entry into the system usually follows a change in income structure rather than a particular postgraduate year.

The ATO works out whether PAYG instalments apply using information from your latest tax return and its published entry thresholds. A few medically relevant scenarios can lead to a first ATO instalment notice.

Locum Income Under an ABN

Locum work paid through an ABN is a common trigger. No PAYG withholding is deducted from contractor payments during the year. If the total tax payable on that income meets the ATO criteria, quarterly instalments may apply in the following financial year.

This is one reason PAYG instalments may arise during registrar training. A doctor combining hospital work and locum income may increase their assessable income and change how tax is collected across the year. Once income extends beyond employer withholding, the collection method may change.

Mixed Hospital Salary and Private Billing Income

Some doctors retain public hospital employment while commencing private billing sessions. Salary from the hospital continues under PAYG withholding. Private billing income is generally received without tax deducted during the year.

The combined income increases the total tax liability. The ATO may introduce instalments once the tax payable on this additional income exceeds its entry thresholds. In this situation, whether PAYG instalments apply can depend more on total taxable income than job title.

One Unusually High Income Year

A single strong income year can also result in PAYG instalments for doctors. This may occur after a year in which income is unusually high for one-off or temporary reasons. The ATO relies on the prior year assessment when determining future quarterly obligations.

If income later reduces, instalments may be varied under ATO rules. The system uses historical figures, which can create timing differences between income and instalment requirements. Awareness of this process reduces confusion when a notice is received.

Investment Income

Non-salary income can trigger entry even where clinical earnings remain consistent. Examples include:

- Rental income from an investment property

- Dividends from listed shares

- Managed fund distributions

Where total tax payable on this additional income reaches ATO thresholds, quarterly instalments may apply. A doctor who begins earning investment income may receive an instalment notice in a later period if the ATO thresholds are met.

Public to Private Transition

A move from public employment into private billing arrangements can alter how tax is collected. Income may no longer flow entirely through payroll withholding. Private practice structures can involve contractor or service, entity models.

A first-year PAYG instalment scenario can follow this transition. Public to private tax discussions often include instalment planning because income composition can become more complex.

Career Stage Comparison

Whether a doctor enters the PAYG instalment system can depend less on career stage itself and more on how income is earned. Doctors earning a salary only through payroll may be less likely to enter the system than those also receiving untaxed locum, private billing, or investment income.

For example, an intern earning only a hospital salary may be less likely to receive a PAYG instalment notice than a doctor whose income also includes ABN or investment income. As income sources become more varied, tax obligations can also become more complex under the ATO’s entry rules.

How PAYG Instalments Are Calculated for Doctors

The ATO provides two main calculation methods: you can pay an instalment amount it calculates for you, or calculate your payment using an instalment rate it gives you. Both approaches rely on your previously lodged tax return. Each is designed to approximate your expected annual tax liability.

Under the instalment amount method, the ATO calculates a fixed quarterly amount based on prior assessed tax payable on business and investment income. This pre-filled figure appears on your activity statement. You can pay that amount as issued or vary it in line with ATO rules if your circumstances have genuinely changed.

Alternatively, the instalment rate method uses a percentage rather than a fixed figure. The ATO provides an instalment rate derived from your previous tax return. You apply this percentage to your instalment income each quarter to determine how much to pay.

To understand how this works in practice, it helps to define instalment income. The ATO states that instalment income is your gross business and investment income, excluding GST. For doctors, this often covers locum income under an ABN and private billing receipts, while salary subject to PAYG withholding is usually excluded.

For many taxpayers, PAYG instalments are due 28 days after the end of each quarter, which often means 28 October, 28 February, 28 April, and 28 July. Depending on the circumstances, the ATO may instead offer two instalments per year or one annual instalment. You report and pay your PAYG instalments through your activity statement or instalment notice.

Once the financial year ends and your tax return is lodged, all PAYG instalments paid are credited against your total assessed tax liability. This reconciliation forms part of your income tax assessment. If instalments exceed the final amount payable, a refund may arise, and if they are insufficient, the remaining balance becomes payable.

A simplified example helps illustrate the process. Consider a registrar earning:

$110,000 hospital salary

$40,000 locum income under an ABN

The hospital salary has PAYG withholding deducted throughout the year, while the $40,000 locum income is received without tax withheld. Total taxable income becomes $150,000 before deductions are applied. When the tax return is assessed, additional tax may be payable on the locum income because no withholding occurred during the year.

If the tax attributable to business and investment income meets ATO entry thresholds, PAYG instalments for junior doctors may commence in the following financial year. This sequence can help explain why PAYG instalments first arise for some doctors. In the next year, the ATO issues quarterly instalments based on that assessed outcome, and each payment is credited against the subsequent income tax assessment.

Are You Paying Tax Twice?

One common concern is whether PAYG instalments mean you are being taxed twice. In general, no. The confusion often follows a predictable pattern:

Year 1 – Extra Income Leads to a Higher Tax Bill

You earn additional income, often through locum work under an ABN or private billing. Tax may not have been withheld from that income during the year. When your tax return is lodged, your higher total income results in a larger tax liability.

Year 2 – The ATO Introduces Quarterly Instalments

After reviewing your income tax assessment, the ATO may enter you into the PAYG instalment system if you meet its published thresholds. This is when many doctors ask: “Do doctors pay PAYG instalments even if tax was already withheld from their hospital salary?” The instalments apply to ongoing business or investment income, not income already subject to PAYG withholding.

End of Year 2 – Instalments are Credited Against Your Tax

When you lodge your next return, every PAYG instalment paid during the year is credited against your total tax payable. If you have overpaid, the excess may be refunded after you lodge your tax return. If you have underpaid, a shortfall may remain.

Can You Vary PAYG Instalments?

Some doctors ask whether they can reduce or vary PAYG instalments once they enter the system. The ATO says you can vary your PAYG instalments if they are too high or too low, including where your expected tax for the current year may be lower than the amount being collected. This may provide relief where income has genuinely changed.

Varying may be appropriate in situations such as:

- Income has materially reduced compared to the previous year

- You have stopped locum work under an ABN

- You are taking parental leave

- You have returned to salary-only employment with PAYG withholding

These scenarios can arise for some junior doctors, particularly during training transitions or family leave. If contractor or private billing income has ceased, projected tax liability may be lower than the instalment amount set by the ATO. In those circumstances, some doctors may consider whether a variation is appropriate under ATO rules.

The ATO allows PAYG instalments to be varied through online services or with the help of a registered tax agent. You are required to estimate your expected tax for the full financial year and adjust instalments accordingly. The varied amount may then replace the original instalment amount or rate for the remaining quarters, depending on the circumstances.

Varying can still carry risk if income is underestimated. Irregular income from locum shifts or private billing can fluctuate across the year. If earnings recover or exceed expectations, the reduced instalments may leave a shortfall.

If your varied instalments are less than 85% of your total tax payable, you may have to pay a general interest charge on the difference, and penalties may also apply depending on the circumstances. The GIC is calculated daily on the shortfall amount and compounds until paid.

Before choosing whether to vary PAYG instalments, it can be useful to review the current year’s income and tax position. The following questions may help frame that review in a general way:

- Has your income materially reduced compared to last year?

- Have you forecast your full-year income, including any private or ABN income?

- Have you considered planned superannuation contributions and deductible expenses?

- Do you understand the potential consequences of underpayment, including GIC?

Variation is part of the PAYG instalment system. It can be used to align quarterly payments more closely to the expected tax liability where circumstances have changed. In that sense, it may affect how tax obligations are managed across the year.

How PAYG Instalments Affect Your Cash Flow as a Doctor

PAYG instalments for doctors influence how and when cash leaves your account. For some junior doctors, income does not arrive in a smooth monthly pattern. This can make planning feel just as important as the tax itself.

Irregular Locum Income

Locum income under an ABN often arrives in larger, less predictable amounts. Hospital salary is usually subject to PAYG withholding, while contractor income may have no tax withheld during the year. This difference can help explain why PAYG instalments may feel abrupt for some locum doctors.

Where PAYG instalments are based on prior year results, they may not align neatly with the current cash flow for doctors with irregular income. A strong run of shifts early in the year can create confidence that later softens. Quarterly instalments remain due regardless of short-term fluctuations.

Quarterly Lump Sum Impact

Unlike payroll deductions, quarterly tax payments require an active transfer of funds. Instalments are due even if the preceding month has been quiet. Without preparation, this can create avoidable pressure.

PAYG instalments vs tax return in Australia timing differences often surprise doctors. The tax is expected during the year rather than after assessment. This requires a more deliberate approach to managing liquidity.

Building a Tax Buffer Account

Setting aside part of irregular income into a separate account can help prepare for upcoming instalments. This can make quarterly payments easier to manage where cash flow is uneven.

Viewing instalments as part of broader cash flow planning can help make quarterly payments feel more manageable. Clear allocation rules may make the process feel more routine and less disruptive.

Coordinating Super Contributions

Eligible personal super contributions may affect taxable income where a deduction is available, and the ATO requirements are met. Coordinating contributions alongside instalments helps avoid overcommitting cash. This becomes particularly relevant during the first year, when PAYG instalments for doctor transitions occur.

Aligning Income Protection Premiums

Income protection premiums can have tax implications depending on the policy structure and individual circumstances. These premiums may also form part of a broader review of annual expenses and taxable income.

Some doctors increase coverage as income rises. Instalments should be considered when adjusting insurance commitments. Cash flow planning can be more effective when protection and tax decisions are reviewed together.

Planning Around Career Transitions

Public to private tax implications for doctor transitions create different timing for tax collection. Moving into private billing or increasing contractor work alters how income is taxed during the year. Instalments frequently follow this change.

Registrars progressing through training may see income rise quickly through additional shifts. Without planning, a higher income one year can create larger instalments the next. Anticipating this pattern supports better financial control.

Should You Vary or Keep Instalments?

PAYG instalments for doctors create a choice once circumstances change. Some doctors may consider whether to vary PAYG instalments, while some may prefer to keep the existing schedule. The decision should be based on current income reality rather than frustration with quarterly payments.

Where income remains consistent with the prior year, keeping instalments may reduce future adjustment. Where earnings have shifted materially, a variation may better reflect expected tax liability. A useful approach is evidence-based forecasting rather than assumptions.

The following checklist can guide structured thinking:

- Has your income materially changed? Consider whether your total expected income differs significantly from the year that triggered the instalments. A genuine reduction in private billing or ABN income may justify review.

- Are you confident in your income forecast? Estimate your likely full-year earnings, including hospital salary, locum income and any other taxable income. Uncertain projections increase the risk of underpayment.

- Are you likely to resume locum shifts? Some doctors reduce contractor work temporarily before returning later in the year. If locum work resumes, lower instalments may create a shortfall.

- Do you have adequate cash reserves? Maintaining instalments can act as a forced saving mechanism. Where cash reserves are strong, keeping instalments may reduce end of year pressure.

- Would professional advice reduce uncertainty? PAYG instalments and annual tax assessments can interact in different ways where income streams vary. The ATO notes that taxpayers who vary instalments need to estimate the tax on their instalment income when working out a varied amount.

ATO confirms that if you vary your PAYG instalments, you need to estimate the tax on your instalment income to work out your varied amount. If instalments are reduced and the final tax payable exceeds the amounts paid, the GIC may apply.

There is no universal answer to whether junior doctors should vary instalments. The appropriate approach may depend on income stability, future work plans and risk tolerance. Before making changes, reviewing the full financial year projection can improve clarity.

Take Control of Your PAYG Instalments

PAYG instalments for doctors can trigger stress, especially during the first year they appear. They are not an extra tax, and they are not a penalty. They are a timing mechanism linked to income growth and changing work structures.

Confidence can come from understanding how PAYG instalments for junior doctors connect to locum income, private billing and career progression. Clarity reduces the fear of getting it wrong. A structured plan replaces guesswork with control.

Income rarely stays static during training and early consultant years. Registrar income can rise quickly, locum work can increase total earnings and public to private transitions can alter tax collection timing. Each change deserves careful planning rather than reactive decisions.

Stronger financial outcomes can be supported by deliberate forecasting and coordinated tax planning. Instalments, super contributions and risk management decisions can be more effective when considered together. A clear strategy turns quarterly payments into a manageable part of your financial system.

If you want more clarity around whether to vary PAYG instalments or keep them in place, it may be a good time to review the numbers carefully. Book a call with Wealthmed and gain clarity on your PAYG instalments and long-term tax strategy.

FAQs

Do junior doctors have to pay PAYG instalments?

Not all junior doctors enter the PAYG instalment system. PAYG instalments for junior doctors usually apply where there is additional untaxed income, such as locum or investment income. If you meet ATO entry thresholds based on your income tax assessment, you may need to pay quarterly instalments.

What income triggers PAYG instalments?

For individuals, including sole traders, the ATO may automatically introduce PAYG instalments where the latest tax return shows instalment income of $4,000 or more, tax payable of $1,000 or more, and estimated or notional tax of $500 or more. Untaxed locum income, private billing income, rent, dividends and managed fund distributions can all contribute, depending on the circumstances.

This can occur when doctors earn ABN income, private billing income or investment income in addition to hospital salary. Mixed-income doctor structures increase the likelihood of receiving an ATO instalment notice.

Can I stop PAYG instalments?

You generally cannot ignore the system once entered, but you may be able to exit PAYG instalments if you are no longer earning business or investment income. You may vary PAYG instalments for doctor obligations if the expected tax for the current year is lower, subject to ATO rules. If income falls below thresholds in future years, the ATO may remove you from the system automatically.

What happens if I ignore the notice?

Ignoring an instalment notice can leave quarterly tax amounts unpaid. The ATO may apply the General Interest Charge in some circumstances, and unpaid obligations can create further compliance issues if they are not addressed.

How often are PAYG instalments due?

PAYG instalments are usually due quarterly. Due dates are published by the ATO and align with standard quarterly reporting periods. Depending on the circumstances, the ATO may require quarterly, twice yearly, monthly, or annual instalments.

Can I switch between the instalment amount and the instalment rate?

The ATO may provide two calculation methods on your activity statement. The instalment amount method uses a fixed quarterly figure, while the instalment rate method applies a percentage to the instalment income. You can choose the method each quarter where both options are available.

Are PAYG instalments refundable?

PAYG instalments are credited against your total tax liability when you lodge your return. If instalments paid exceed the final tax payable, the excess may be refunded. This is part of the PAYG instalments vs tax return Australia reconciliation process.

Do interns usually pay PAYG instalments?

Interns earning only a public hospital salary are typically subject to PAYG withholding through payroll. Without additional untaxed income, they are less likely to enter the instalment system. Entry depends on the total tax payable and ATO thresholds.

What is the General Interest Charge?

Based on ATO, the General Interest Charge applies to unpaid tax liabilities and is worked out daily on a compounding basis, which means the amount owing can grow over time. In the context of PAYG instalments, it may apply if instalments are paid late or if they have been reduced too far and a shortfall arises.

Disclaimer: The information contained in this blog/newsletter is general in nature and has been prepared without taking into account your personal objectives, financial situation or needs.

Wealthmed’s financial planning services are provided by Eureka Financial Group Pty Ltd as an authorised representative of Fortnum Advice Pty Ltd (ABN 52 634 060 709; AFSL 519190). Lending and mortgage-broking services are provided by Wealthmed as a credit representative of Yarra Lane Finance Pty Ltd (Australian Credit Licence 39227).

Accounting and tax services are delivered by Wealthmed Accounting Pty Ltd (Tax Agent No 24677924) as a separate entity and are not financial services under the AFSL. Nothing in this publication constitutes financial, legal or tax advice. You should seek professional advice relevant to your individual circumstances before making any financial decisions.